The National Stabilization Fund earned a return of 81 percent on stocks it purchased during its latest market intervention from April 9 last year to Jan. 12, the Ministry of Finance said on Monday.The results were released by the management committee of the stabilization fund, which was set up to ea

As a global race to build artificial intelligence (AI) infrastructure reshapes investment flows and supply chains, Citigroup Inc is positioning Taiwan as a key market in its strategy to capture rising demand for cross-border banking, capital markets and advisory services.The US banking giant sees Ta

Landis Hotels & Resorts Corp (亞都麗緻) is on track for a recovery in the second half of the year as a rebound in international business travel and resilient premium dining demand help strengthen its earnings outlook.The hotel operator posted first-half revenue of NT$252 million (US$7.83 million), up 15

Formosa Plastics Group (FPG, 台塑集團) has decided to raise wages for its employees by 4.5 percent this year, exceeding the 3.66 percent raise requested by the group’s worker union.Speaking with reporters, Chen Hung-ju (陳鴻儒), deputy head of the FPG workers’ union, said the decision was made after a meet

Taiwan’s approved outbound investment rose nearly 58 percent over the past five years as companies accelerated efforts to diversify production and supply chains beyond China, with the US and Southeast Asia emerging as the top manufacturing destinations, the Ministry of Economic Affairs (MOEA) said y

United Microelectronics Corp (UMC, 聯電), the second largest contract chipmaker in Taiwan, said yesterday that it has started mass production of silicon photonics wafers at its 12-inch wafer fab in Singapore.The first batch of silicon photonics wafers in commercial production was achieved in collabora

SoftBank Robotics Corp’s Mini Pepper robot is displayed at the SoftBank World forum in Tokyo yesterday. SoftBank Group founder Masayoshi Son said that in the near future, nuclear fusion technology will offer the most realistic solution for powering AI data centers’ ballooning requirements.

MOMENTUM: Second-quarter revenue reached NT$1.27 trillion as the June turnover surged, while TSMC’s 2nm process spending and US expansion remain focus points

Taiwan Semiconductor Manufacturing Co (TSMC, 台積電) yesterday reported its highest quarterly sales amid strong global demand for artificial intelligence (AI) applications.The world’s largest contract chipmaker posted NT$1.27 trillion (US$39.5 billion) in consolidated revenue for the second quarter of

STRATEGIC PUSH: The lender invested NT$100 million in the outlet to expand private banking and family office services for high-net-worth clients

CTBC Bank Co (中信銀行) yesterday inaugurated its Asia New Bay Area branch in Kaohsiung, positioning the facility as a strategic hub to support Taiwan’s emerging asset management center and expand its wealth management services for high-net-worth clients. It is the bank’s 159th outlet nationwide and its

China Steel Corp (CSC, 中鋼), Taiwan’s largest integrated steelmaker, yesterday announced that it would cut steel prices by NT$800 per tonne across the board for domestic delivery next month, a larger reduction than the NT$300 reduction for this month’s deliveries.The price cuts cover products ranging

Lite-On Technology Corp (光寶科技) yesterday said it would invest US$919 million to establish a manufacturing facility in McKinney, Texas.US$108.5 million of this would be used to acquire factory buildings, Lite-On said in a statement.The McKinney site, spanning more than 650,000 square feet (60,387 squ

Taiwanese consumers expect their cost of living to rise by an average of 8.77 percent over the next year, reflecting growing inflation concerns, even before higher inflation becomes evident in official data, a survey released yesterday by Academia Sinica showed. The Institute of Economics at Academi

A man dries “Guanmiao noodles” in the sun in Tainan yesterday. The weather in Tainan has been sunny after Typhoon Bavi moved away from Taiwan, and local noodle makers are gearing up to produce the well-known sun-dried noodles, the Guanmiao District Farmers’ Association said yesterday.

TECH CORRIDOR: The new Phase II site is expected to work with other facilities in the region and nation as TSMC looks to shape the future with its manufacturing

Taiwan Semiconductor Manufacturing Co (TSMC, 台積電) would build three additional advanced packaging facilities in Phase II of the Chiayi Science Park (嘉義科學園區), National Science and Technology Council (NSTC) Minister Wu Cheng-wen (吳誠文) said yesterday.Speaking at the groundbreaking ceremony for the Phas

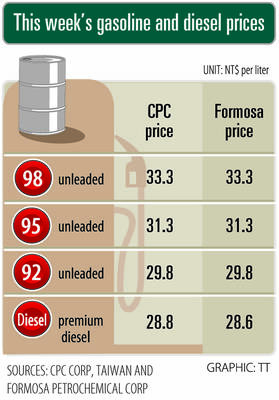

CPC Corp, Taiwan (CPC, 台灣中油) announced on Saturday that it would keep its domestic gasoline and diesel prices unchanged this week despite a spike in international crude oil prices last week.Formosa Petrochemical Corp (台塑石化) yesterday said it would also maintain fuel prices at the same level this wee

SK Group chairman Chey Tae-won, fresh off a landmark US stock offering for the conglomerate’s memorychip business, said he has an ambitious plan to invest more money in America.SK Group is already putting more than US$35 billion into the US, Chey said on Friday in an interview with Bloomberg Televis

THE NEWEST, THE SHINIEST: A younger client base prioritizes smart-driving and digital features as they rapidly replace EVs that are no longer cutting-edge

Chinese electric vehicles (EVs) on the road are on average just 1.8 years old, compared with 8.2 years for gasoline-powered cars, 21st Century Business Herald said, citing a report by the China Association of Automobile Manufacturers (CAAM) and Hejun Consulting Co (和君諮詢).The newspaper said the figur

Despite a year of searching, stints at big automotive suppliers and sending out about 50 applications, German software engineer Max Peil is still looking for a job.Trained in computer vision, a critical part of autonomous and intelligent driving systems, Peil could once have expected to cruise into

People buy mangoes at a wholesale market in Tainan’s Yujing District yesterday after Typhoon Bavi moved away from Taiwan. With the Irwin mango harvest season nearing its end, reduced output and strong demand has led the average mango price to climb to NT$67.4 per kg from about NT$35 at the beginning