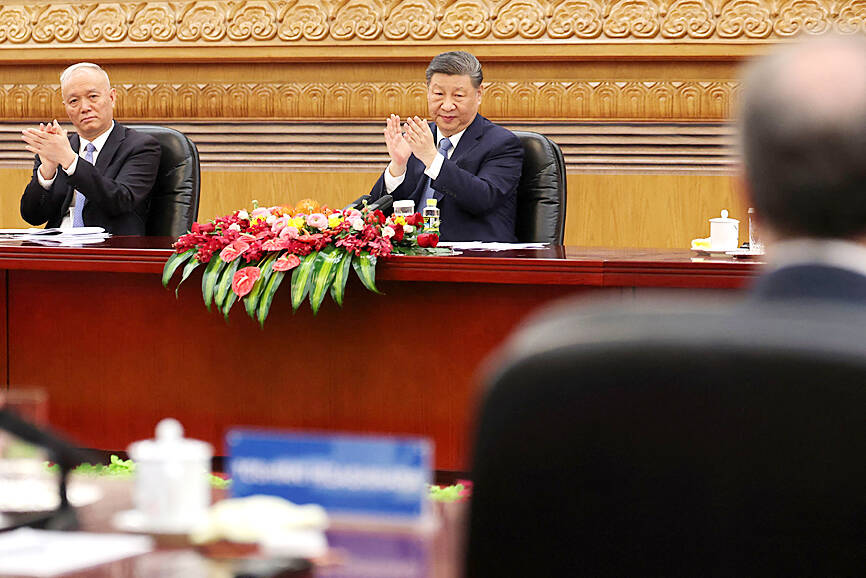

Chinese President Xi Jinping (習近平) yesterday met with a group of global business leaders in Beijing in an effort to boost investor sentiment as rising tariffs fuel uncertainty about the economy and international trade.

Xi sat down with representatives of international industrial and business firms at the Great Hall of the People in Beijing yesterday morning, Xinhua news agency reported, without elaborating.

They included Rajesh Subramaniam of FedEx Corp, Bill Winters of Standard Chartered PLC, Paul Hudson of Sanofi SA, Pascal Soriot of AstraZeneca PLC and Miguel Angel Lopez Borrego of ThyssenKrupp AG.

Photo: Reuters

Officials in attendance included Chinese Minister of Foreign Affairs Wang Yi (王毅), Minister of Commerce Wang Wentao (王文濤) and Minister of Finance Lan Foan (藍佛安).

After the meeting, Xi said in front of reporters that seven business representatives shared their views that the Chinese government would “study and consider.”

“All of you are welcome to keep your lines of communication with us,” Xi said, praising the attendees for contributing to China’s growth and creating job opportunities.

“Foreign businesses are important participants in China’s modernization,” he added.

Slowing economic expansion and mounting geopolitical tensions have hurt the appeal of investing in the world’s second-biggest economy, with inbound investment tumbling last year to its lowest in more than three decades.

More headwinds might come next month, when the US is set to complete a review of Beijing’s compliance with the phase-one trade deal struck during US President Donald Trump’s first term and impose reciprocal duties globally.

Chinese Premier Li Qiang (李強) on Sunday said that the country is prepared for “shocks that exceed expectations,” as the government targets an ambitious growth target of about 5 percent this year.

Economists estimate that Beijing would need to unleash trillions of yuan in stimulus to hit that goal if tariffs surge.

China’s interaction with the top business figures underscores the message it has been sending that the nation is open for business — contrasting itself with Trump’s more protectionist “America first” policies.

Beijing is also trying to cast itself as a supporter of private enterprise, illustrated by Xi’s meeting last month with entrepreneurs such as Alibaba Group Holding Ltd (阿里巴巴) cofounder Jack Ma (馬雲).

Many global chief executive officers had traveled to China for the annual China Development Forum and the Boao Forum for Asia, which concluded yesterday.

The meeting marked an upgrade from earlier years when China’s No. 2 official met executives on the sidelines of the China Development Forum, although Xi broke precedent last year to meet with a group of US businesspeople.

US Senator Steve Daines, a member of the Senate Foreign Relations Committee, met with several Chinese leaders, including Li, earlier this week, in what has been seen as an initial step to set up a summit between Xi and Trump.

Several US firms have already been caught in the crossfire of deteriorating bilateral relations.

Chinese authorities summoned Walmart Inc executives this month over reports it asked suppliers to bear rising costs incurred by increased US tariffs.

Beijing earlier placed Calvin Klein owner PVH Corp and US gene sequencing company Illumina Inc onto a so-called blacklist of entities as US tariffs took effect.

ENERGY ISSUES: The TSIA urged the government to increase natural gas and helium reserves to reduce the impact of the Middle East war on semiconductor supply stability Chip testing and packaging service provider ASE Technology Holding Co (日月光投控) yesterday said it planned to invest more than NT$100 billion (US$3.15 billion) in building a new advanced chip testing facility in Kaohsiung to keep up with customer demand driven by the artificial intelligence (AI) boom. That would be included in the company’s capital expenditure budget next year, ASE said. There is also room to raise this year’s capital spending budget from a record-high US$7 billion estimated three months ago, it added. ASE would have six factories under construction this year, another record-breaking number, ASE chief operating officer Tien Wu

The EU and US are nearing an agreement to coordinate on producing and securing critical minerals, part of a push to break reliance on Chinese supplies. The potential deal would create incentives, such as minimum prices, that could advantage non-Chinese suppliers, according to a draft of an “action plan” seen by Bloomberg. The EU and US would also cooperate on standards, investments and joint projects, as well as coordinate on any supply disruptions by countries like China. The two sides are additionally seeking other “like-minded partners” to join a multicountry accord to help create these new critical mineral supply chains, which feed into

For weeks now, the global tech industry has been waiting for a major artificial intelligence (AI) launch from DeepSeek (深度求索), seen as a benchmark for China’s progress in the fast-moving field. More than a year has passed since the start-up put Chinese AI on the map in early last year with a low-cost chatbot that performed at a similar level to US rivals. However, despite reports and rumors about its imminent release, DeepSeek’s next-generation “V4” model is nowhere in sight. Speculation is also swirling over the geopolitical implications of which computer chips were chosen to train and power the new

Intel Corp is joining Elon Musk’s long-shot effort to develop semiconductors for Tesla Inc, Space Exploration Technologies Corp and xAI, marking a surprising twist in the chipmaker’s comeback bid. Intel would help the Terafab project “refactor” the technology in a chip factory, the company said on Tuesday in a post on X, Musk’s social media platform. That is a stage in the development process that typically helps make chips more powerful or reliable. The chipmaker’s shares jumped 4.2 percent to US$52.91 in New York trading on Tuesday. The Terafab project is a grand plan by Musk to eventually manufacture his own chips for