Venezuela has awarded a stake in a key oil joint venture to a little-known firm called GazMin International Group almost six months after seizing it from Russian executives, people with direct knowledge of the matter said.

Gazmin now has a 40 percent holding in Petrozamora SA, while state oil company Petroleos de Venezuela SA holds the other 60 percent, said the people, who asked not to be identified as the decision has not been formally announced.

The minority stake was previously owned by GPB Global Resources, a closely held energy firm founded by former Gazprom PJSC officials, the people said.

Photo: Reuters

Venezuelan President Nicolas Maduro’s government in September last year took over Petrozamora in the hopes of controlling its exports directly, the people said.

At the time, GPB called the move an “illegal asset expropriation.”

Gazmin says on its Web site that it is based in the United Arab Emirates and Kuwait.

Some of its partners are Venezuelan nationals, the people said.

The United Arab Emirates’ federal registry shows a firm named GazMin was formed in September 2019, although it is not clear if that’s the same entity doing business in Venezuela. PDVSA and GPB did not respond to requests for comment.

The changes in ownership follow a tumultuous time for the global oil market and Venezuela’s place in it. The country has lost out to cheaper Russian crude in the Chinese market, which in preceding years has been one of the biggest buyers of oil from the South American nation. Russian oil has been sold at a discounted price amid efforts by the US and other G7 nations to curb Moscow’s energy revenues.

That is not the only recent change for Venezuelan exports. Chevron Corp is now able to export from the country to the US after the easing of sanctions targeting the Maduro government. Venezuela could soon be sending more oil to the US than Persian Gulf producers Kuwait and Libya combined.

Prior to US sanctions, Petrozamora was one of the most productive oil ventures in Venezuela, with all of its crude going to Europe.

Meanwhile, oil fell as macroeconomic headwinds dominate the market, while traders wait and see how demand pans out.

West Texas Intermediate for April delivery on Friday rose 1.27 percent to US$76.68 a barrel, but declined 3.77 percent this week amid fears that recent economic data would impel the US Federal Reserve to more aggressively raise interest rates, compounding pressure from China’s tempered economic projections.

Brent crude for April delivery gained 1.46 percent to US$82.78 a barrel, but posted a weekly loss of 3.55 percent.

Any bulls looking for a bump in prices from the supply side have so far been disappointed by resilient flows from Russia counteracting recent concerns of the longevity of the growth in US supply.

“Risk appetite is dominating as crude traders shy away from substantially increasing their positioning with prices locked into a tight range,” TD Securities commodity strategist Daniel Ghali, said.

Additional reporting by staff writer

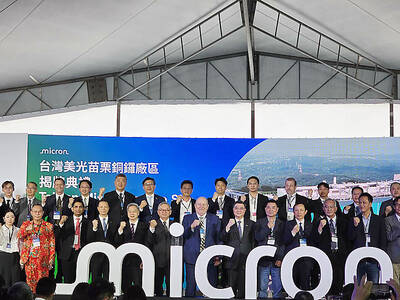

UNPRECEDENTED PACE: Micron Technology has announced plans to expand manufacturing capabilities with the acquisition of a new chip plant in Miaoli Micron Technology Inc unveiled a newly acquired chip plant in Miaoli County yesterday, as the company expands capacity to meet growing demand for advanced DRAM chips, including high-bandwidth memory chips amid the artificial intelligence boom. The plant in Miaoli County’s Tongluo Township (銅鑼), which Micron acquired from Powerchip Semiconductor Manufacturing Corp (力積電) for US$1.8 billion, is expected to make a sizeable capacity contribution to the company from fiscal 2028, the company said in a statement. It would be an extended production site of Micron’s large-scale manufacturing hub in Taichung, the company said. As the global semiconductor industry is racing to reach US$1 trillion

Singapore-based ride-hailing and delivery giant Grab Holdings Ltd has applied for regulatory approval to acquire the Taiwan operations of Germany-based Delivery Hero SE's Foodpanda in a deal valued at about US$600 million. Grab submitted the filing to the Fair Trade Commission on Friday last week, with the transaction subject to regulatory review and approval, the company said in a statement yesterday. Its independent governance structure would help foster a healthy and competitive market in Taiwan if the deal is approved, Grab said. Grab, which is listed on the NASDAQ, said in the filing that US-based Uber Technologies Inc holds about 13 percent of

ABOVE LEGAL REQUIREMENT: The Ministry of Economic Affairs is prepared if LNG supply is disrupted, with more than the legal requirement of 11 days of inventory Taiwan has largely secured liquefied natural gas (LNG) supplies through May and arranged about half of June’s supply, Minister of Economic Affairs Kung Ming-hsin (龔明鑫) said yesterday. Since the Middle East conflict began on Feb. 28, Taiwan’s LNG inventories have remained more than 12 days, exceeding the legal requirement of 11 days, indicating no major supply concerns for domestic gas and electricity, Kung said at a meeting of the legislature’s Economics Committee in Taipei. The ministry aims to increase the figure to 14 days by the end of next year, he said. While one or two LNG or crude oil shipments for May

Taiwan’s food delivery market could undergo a major shift if Singapore-based Grab Holdings Ltd completes its planned acquisition of Delivery Hero SE’s Foodpanda business in Taiwan, industry experts said. Grab on Monday last week announced it would acquire Foodpanda’s Taiwan operations for US$600 million. The deal is expected to be finalized in the second half of this year, with Grab aiming to complete user migration to its platform by the first half of next year. A duopoly between Uber Eats and Foodpanda dominates Taiwan’s delivery market, a structure that has remained intact since the Fair Trade Commission (FTC) blocked Uber Technologies Inc’s