European stocks fell, trimming their fourth straight weekly advance, as a surge in US unemployment to a 25-year high damped optimism that the worst of the global recession is over.

Credit Suisse Group AG and Deutsche Bank AG slid more than 1.8 percent as a report showed employers in America cut 663,000 jobs last month.

Novo Nordisk AS tumbled 14 percent after the drugmaker’s experimental diabetes shot received a split recommendation from a US advisory panel. Renault SA and Daimler AG led automakers higher as Credit Suisse upgraded the industry to “overweight.”

“We have a very awful, deep recession,” Jan Loeys, JPMorgan Chase & Co’s global head of market strategy, said in a Bloomberg Television interview in London.

“At some point we will be turning around, but the question is: Is it this year or next year?” Loeys said.

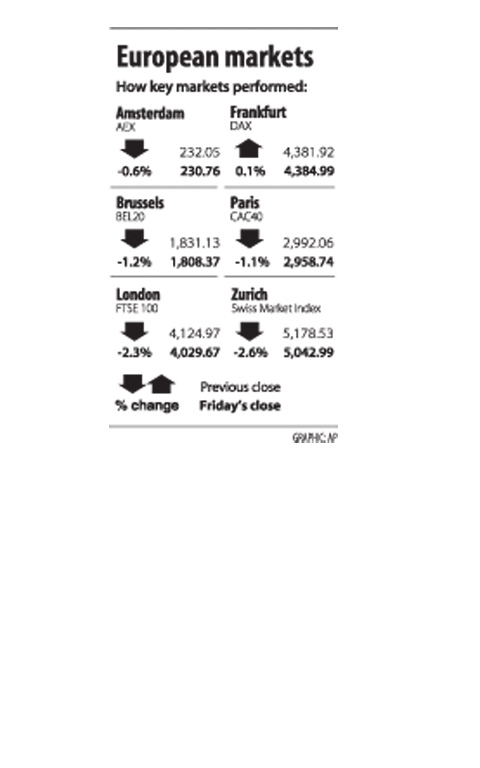

The Dow Jones STOXX 600 Index slid 1 percent to 186.17. The measure posted its fourth week of gains, the longest streak since the global bear market that wiped out US$37 trillion of equity value began in October 2007.

The benchmark index for European stocks has climbed 18 percent since March 9 as the biggest US banks said they made money in the first two months of this year and US Treasury Secretary Timothy Geithner unveiled plans to finance as much as US$1 trillion in purchases of banks’ distressed assets.

National benchmark indexes retreated in 14 of the 18 western European markets. France’s CAC 40 lost 1.1 percent and Germany’s DAX added 0.1 percent. The UK’s FTSE 100 sank 2.3 percent as Tesco PLC retreated.

Financial shares rallied this week as the US Financial Accounting Standards Board agreed to relax fair-value, or mark-to-market, accounting that requires banks to revalue assets each quarter to reflect market prices. Writedowns and credit-related losses at financial institutions have swelled to US$1.29 trillion since the start of 2007.

“You still want to be quite cautious,” said Paul Kavanagh, a partner at Killik & Co in London, which has about US$2.9 billion in assets under management.

“It’s far too early to start thinking about a recovery in the economy,” he said.

MORE VISITORS: The Tourism Administration said that it is seeing positive prospects in its efforts to expand the tourism market in North America and Europe Taiwan has been ranked as the cheapest place in the world to travel to this year, based on a list recommended by NerdWallet. The San Francisco-based personal finance company said that Taiwan topped the list of 16 nations it chose for budget travelers because US tourists do not need visas and travelers can easily have a good meal for less than US$10. A bus ride in Taipei costs just under US$0.50, while subway rides start at US$0.60, the firm said, adding that public transportation in Taiwan is easy to navigate. The firm also called Taiwan a “food lover’s paradise,” citing inexpensive breakfast stalls

TRADE: A mandatory declaration of origin for manufactured goods bound for the US is to take effect on May 7 to block China from exploiting Taiwan’s trade channels All products manufactured in Taiwan and exported to the US must include a signed declaration of origin starting on May 7, the Bureau of Foreign Trade announced yesterday. US President Donald Trump on April 2 imposed a 32 percent tariff on imports from Taiwan, but one week later announced a 90-day pause on its implementation. However, a universal 10 percent tariff was immediately applied to most imports from around the world. On April 12, the Trump administration further exempted computers, smartphones and semiconductors from the new tariffs. In response, President William Lai’s (賴清德) administration has introduced a series of countermeasures to support affected

CROSS-STRAIT: The vast majority of Taiwanese support maintaining the ‘status quo,’ while concern is rising about Beijing’s influence operations More than eight out of 10 Taiwanese reject Beijing’s “one country, two systems” framework for cross-strait relations, according to a survey released by the Mainland Affairs Council (MAC) on Thursday. The MAC’s latest quarterly survey found that 84.4 percent of respondents opposed Beijing’s “one country, two systems” formula for handling cross-strait relations — a figure consistent with past polling. Over the past three years, opposition to the framework has remained high, ranging from a low of 83.6 percent in April 2023 to a peak of 89.6 percent in April last year. In the most recent poll, 82.5 percent also rejected China’s

PLUGGING HOLES: The amendments would bring the legislation in line with systems found in other countries such as Japan and the US, Legislator Chen Kuan-ting said Democratic Progressive Party (DPP) Legislator Chen Kuan-ting (陳冠廷) has proposed amending national security legislation amid a spate of espionage cases. Potential gaps in security vetting procedures for personnel with access to sensitive information prompted him to propose the amendments, which would introduce changes to Article 14 of the Classified National Security Information Protection Act (國家機密保護法), Chen said yesterday. The proposal, which aims to enhance interagency vetting procedures and reduce the risk of classified information leaks, would establish a comprehensive security clearance system in Taiwan, he said. The amendment would require character and loyalty checks for civil servants and intelligence personnel prior to