South Korea’s jobless rate surged to its highest in more than two decades, raising concern that an export-driven recovery could be masking a harsher scarring of the economy.

The unemployment rate jumped to 5.4 percent last month from a revised 4.5 percent in December last year, hitting its highest level since after the Asian financial crisis.

The result outstripped all forecasts as the economy shed almost 1 million jobs from a year earlier for the worst losses since 1998.

The sharp deterioration in the labor market contrasts with the view that the South Korean economy has been one of the best performers in the developed world last year and suggests that the South Korean government might need to take more action to support jobs.

“The huge hit to jobs is going to weigh on the pace of economic recovery,” said Sung Tae-yoon, an economics professor at Yonsei University in Seoul. “People looking for jobs will also decrease as the economy worsens, which may technically bring down the jobless rate, but economic difficulties will continue.”

Last month, the sector combining retailers, wholesalers, restaurants and hotels was hit hardest with 585,000 job losses from a year earlier.

More than 340,000 positions were shed in a sector that includes public service, as the government’s job-creation measures expired. Manufacturing lost 46,000 jobs.

The government takes the situation “seriously” and would use all available options to deal with it, South Korean Minister of Finance Hong Nam-ki said in a statement, blaming the job losses partly on expired fiscal support for jobs creation at the turn of the year, and a high year-earlier base.

South Korean President Moon Jae-in is also calling for incentives for companies that would share some of their profits during the pandemic with ones that were hit harder, a move that could indirectly support employment.

Some South Korean lawmakers are putting pressure on the Bank of Korea to adopt a jobs mandate as part of its goals.

SECOND-RATE: Models distilled from US products do not perform the same as the original and undo measures that ensure the systems are neutral, the US’ cable said The US Department of State has ordered a global push to bring attention to what it said are widespread efforts by Chinese companies, including artificial intelligence (AI) start-up DeepSeek (深度求索), to steal intellectual property from US AI labs, according to a diplomatic cable. The cable, dated Friday and sent to diplomatic and consular posts around the world, instructs diplomatic staff to speak to their foreign counterparts about “concerns over adversaries’ extraction and distillation of US AI models.” Distillation is the process of training smaller AI models using output from larger, more expensive ones to lower the costs of training a powerful new

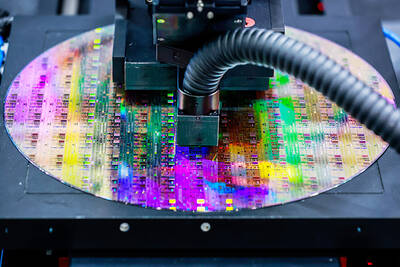

Shares of Taiwan Semiconductor Manufacturing Co (TSMC, 台積電) have repeatedly hit new highs, but an equity analyst said the stock’s valuation remains within a reasonable range and any pullback would likely be technical. The contract chipmaker’s historical price-to-earnings (P/E) ratio has ranged between 20 and 30, Cathay Futures Consultant Co (國泰證期) analyst Tsai Ming-han (蔡明翰) told Central News Agency. With market consensus projecting that TSMC would post earnings per share of about NT$100 (US$3.17) this year, supported by strong global demand for artificial intelligence (AI) applications, and the stock currently trading at a P/E ratio of below 25, Tsai said the valuation

The artificial intelligence (AI) boom has triggered a seismic reshuffling of global equity markets, with Taiwan and South Korea muscling past European nations one by one. With its stock market now valued at nearly US$4.3 trillion, Taiwan surpassed the UK, Europe’s biggest market, earlier this month, data compiled by Bloomberg showed. South Korea is about US$140 billion away from doing the same. The tech-heavy Asian markets have shot past Germany and France in the past seven months. The shift is largely down to massive gains in shares of three companies that provide essential hardware for AI: Taiwan Semiconductor Manufacturing Co (TSMC, 台積電),

The US Department of Commerce last week ordered multiple chip equipment companies to halt shipments of certain tools to China’s second-largest chipmaker, Hua Hong Semiconductor Ltd (華虹半導體), its latest action to slow the country’s development of advanced chips, two people familiar with the matter said. The department sent letters to at least a handful of companies informing them of restrictions on tools and other materials destined for two Hua Hong facilities US officials believe make China’s most sophisticated chips, the people said. Top US chip equipment companies Lam Research Corp, Applied Materials Inc and KLA Corp, each of which has significant