The chief executive of trouble-plagued German lender Deutsche Bank AG has written to employees to dash rumors he would soon be pushed out, saying he was “absolutely committed” to righting the bank.

“I am absolutely committed to serving our bank and to continuing down the path” back to stability and profitability, John Cryan wrote in a letter late on Wednesday.

While Cryan’s contract runs until 2020, press reports in recent days have suggested a rift over strategy with supervisory board chairman Paul Achleitner, who is said to be seeking a replacement.

Given sole command of the lender in 2016, Cryan’s task was to restructure Deutsche and clean up the toxic legacy of its pre-financial crisis bid to compete with global investment banking giants.

He has neutralized the worst legal threats, in part by paying billions in fines and compensation, strengthened Deutsche’s capital foundations with an 8 billion euro (US$9.9 billion) share issue last year and floated asset management division DWS on the stock market this month.

“The financial results have so far not been what all of us would want them to be,” Cryan wrote, in a nod to an unexpected 751 million euro loss reported for last year.

While the bank said the loss was a one-off caused by US President Donald Trump’s corporate tax reform, investors have shunned Deutsche since the start of the year, with its stock dropping around 30 percent in value since Jan. 1.

Nevertheless, “we need to focus on executing the strategy that was agreed and signed off by both the management and supervisory boards,” Cryan said in a bid to smooth over the reported divisions at the top. “There is no difference of opinion here.”

Looking ahead “I personally have to give the company direction as we have to rebalance the often conflicting demands of our various stakeholders,” Cryan said.

As Deutsche moves out of its intensive-care phase there will be “more emphasis on generating attractive shareholder returns and returning to growth,” he added.

Merida Industry Co (美利達) has seen signs of recovery in the US and European markets this year, as customers are gradually depleting their inventories, the bicycle maker told shareholders yesterday. Given robust growth in new orders at its Taiwanese factory, coupled with its subsidiaries’ improving performance, Merida said it remains confident about the bicycle market’s prospects and expects steady growth in its core business this year. CAUTION ON CHINA However, the company must handle the Chinese market with great caution, as sales of road bikes there have declined significantly, affecting its revenue and profitability, Merida said in a statement, adding that it would

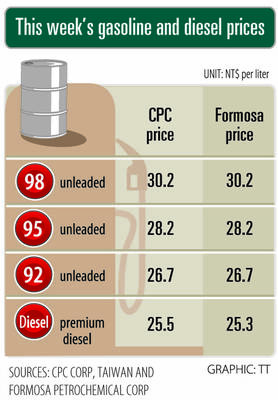

i Gasoline and diesel prices at fuel stations are this week to rise NT$0.1 per liter, as tensions in the Middle East pushed crude oil prices higher last week, CPC Corp, Taiwan (台灣中油) and Formosa Petrochemical Corp (台塑石化) said yesterday. International crude oil prices last week rose for the third consecutive week due to an escalating conflict between Israel and Iran, as the market is concerned that the situation in the Middle East might affect crude oil supply, CPC and Formosa said in separate statements. Front-month Brent crude oil futures — the international oil benchmark — rose 3.75 percent to settle at US$77.01

RISING: Strong exports, and life insurance companies’ efforts to manage currency risks indicates the NT dollar would eventually pass the 29 level, an expert said The New Taiwan dollar yesterday rallied to its strongest in three years amid inflows to the nation’s stock market and broad-based weakness in the US dollar. Exporter sales of the US currency and a repatriation of funds from local asset managers also played a role, said two traders, who asked not to be identified as they were not authorized to speak publicly. State-owned banks were seen buying the greenback yesterday, but only at a moderate scale, the traders said. The local currency gained 0.77 percent, outperforming almost all of its Asian peers, to close at NT$29.165 per US dollar in Taipei trading yesterday. The

RECORD LOW: Global firms’ increased inventories, tariff disputes not yet impacting Taiwan and new graduates not yet entering the market contributed to the decrease Taiwan’s unemployment rate last month dropped to 3.3 percent, the lowest for the month in 25 years, as strong exports and resilient domestic demand boosted hiring across various sectors, the Directorate-General of Budget, Accounting and Statistics (DGBAS) said yesterday. After seasonal adjustments, the jobless rate eased to 3.34 percent, the best performance in 24 years, suggesting a stable labor market, although a mild increase is expected with the graduation season from this month through August, the statistics agency said. “Potential shocks from tariff disputes between the US and China have yet to affect Taiwan’s job market,” Census Department Deputy Director Tan Wen-ling