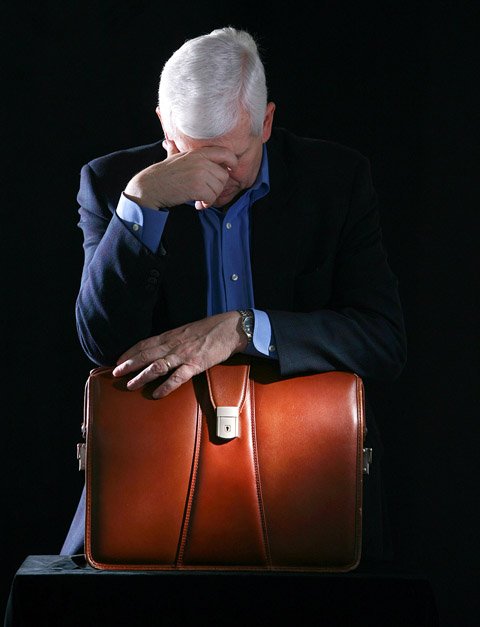

The mind wraps itself around losing a job, one of life's great traumas, in jagged and swerving fits. When the call comes in, when rumor turns to reality, when it's not the broker in the next cubicle but you who are presented with a stack of severance papers, the psyche takes over.

It goes numb. It goes into survival mode. Fear quickly turns into anger. For some, there may be relief in saying goodbye to what therapists call the “psychological terror” that has haunted the corridors of troubled financial institutions since last summer. But what follows — the unknown — may be no less frightening.

Since August, banks worldwide have announced plans to eliminate as many as 65,000 jobs. Many losing their jobs now have lived through other crises on Wall Street — the 1987 market crash, the widespread layoffs of the early 1990s and the financial upheaval of 1998. But investment bankers, recruiters and psychologists say the current economic downturn, the cascade of layoffs and the steady beat of grim financial news have exacted an especially daunting psychic price.

PHOTO: NY TIMES NEWS SERVICE

“These are people’s lives,” said an investment banker in his 30s who was laid off in November from his job at a Bank of America office in New York. “It’s not head count. We’re not cattle.”

Like other employees interviewed for this article, the Bank of American employee spoke on the condition of anonymity. He and several others who were laid off said that under the terms of their severance packages, they are not permitted to sue the company or to speak out negatively about it.

In an e-mail message, Bank of America said: “Job reductions are sometimes a necessary course of business, but they are never easy, whether you are receiving the message or delivering it. We always try to be as respectful as possible.”

PHOTO: NY TIMES NEWS SERVICE

Even for some of those who survive a job cut, the emotional landscape can change.

“It’s like I woke up and I’m in a different country,” said a person who has worked for Merrill Lynch for more than two decades and has weathered a recent round of layoffs there.

He described widespread anger, mistrust and angst at Merrill, both among those leaving and those staying.

“People are reeling,” he said. “The culture has turned. It is a nasty culture.”

Merrill Lynch laid off 20,000 people in the wake of the Sept. 11 terrorist attacks, and while many Wall Street workers say the deaths of co-workers were a shattering experience, they draw a distinction between banks’ actions then and now. Merrill has laid off 4,000 employees this year. In this round, “these were self-inflicted wounds,” the Merrill employee said.

The Merrill banker spoke on the condition of anonymity, saying the company does not permit employees to speak to reporters without permission, and he said he feared retribution if he sought that permission or identified himself.

Officials at Merrill Lynch declined to comment.

Among the patients who have seen Alden Cass, a psychologist who treats Wall Street traders and executives, are several who were laid off from Bear Stearns after the bank collapsed.

“They felt as if they were led with blindfolds on into a firing squad,” Cass said.

Officials at JPMorgan Chase & Co, which is acquiring Bear Stearns, declined to comment.

Cass and other psychologists and researchers who have worked with Wall Street employees say that these workers — often drawn to the intensity and volatility of their profession — are more prone to anxiety, depression, substance abuse and other mental stresses than the general population. They drive themselves hard. Working 10, 12, 14 hours a day is not only expected; it is also a badge of honor.

In some ways, these experts say, Wall Street types are perhaps better prepared to handle the shock of sudden change than those in more stable professions. But because they are typically measured by the size of their paycheck — bonuses, in particular — their self-worth is deeply threatened when the money evaporates.

“We’re talking about individuals who base their identities and egos on what they do for a living and how much they make,” Cass said.

Yet Wall Street is also a macho, “don’t let them see you sweat” world where showing self-doubt and weakness, whether to clients or co-workers, is about as welcome as a stock whose value is taking a nosedive.

Still, psychologists say, for those being laid off, whether or not they are comfortable expressing it, there is boiling anger, a sense of betrayal and loss that is bound to rise to the surface.

That appears to be true for the former investment banker at Bank of America who talked about being treated like cattle. He said he went numb when he was brought into a conference room with his manager and told he was being let go. He would get no bonus for last year either, typically 40 percent of his US$120,000 annual salary, he said, and he was offered eight weeks of severance pay, which he accepted.

“I had no emotional response,” he said.

Yet he is clearly angry now.

“Someone who shows up to work every day, that should engender some sense of loyalty,” he said.

He was at Morgan Stanley in 1998, when it and other Wall Street banks were laying off thousands of workers. He had joined the bank in 1997, and before the layoffs, he said: “There was a sense of loyalty, they got my back, that sense of pride.”

“But that loyalty idea is gone for most of these banks,” he said.

He had been with Bank of America for three-and-a half years when the layoff rumors, swirling in his department for weeks, reached a high pitch. Since October, the bank has cut 1,150 jobs.

He looked for work for six months, ran through his savings and recently found consulting work. He is single, rents a unit in Manhattan and is still paying off loans from business school, as well as several thousand dollars of credit card debt.

He says he decided to stick to consulting because he no longer believes he can rely on bonuses or the guarantee of a long-term full-time job. With the layoffs, he said, the banks are “destroying their greatest assets. It’s an us-against-them mentality now.”

A 50-year-old Merrill financial adviser had already survived the 1987 stock market crash and crushing waves of layoffs before the Bank of America employee had even graduated from business school. For him, the layoffs at Merrill were not surprising, and the opportunity he took this month for a buyout felt like a gift.

He said that because Merrill would not authorize an interview, he did not want to be identified and risk jeopardizing the package, which provided him with 67 weeks of pay on a US$101,000 salary and to stay on the firm’s health plan, paying out of pocket about US$400 more per month than he did when he was with Merrill. He said he was sometimes irked by media coverage describing the layoffs as shocking and devastating.

“If you went to school and you studied this industry and you studied economic cycles, why are you now surprised that this is happening?” he said. “It’s like going into politics and saying, ‘I didn’t know I could be voted out of office.”’

He described himself as very cautious in his own financial affairs and said he began planning for retirement early in life.

“I’m in financial planning,” he said. “Isn’t it a sin not to do so for yourself?”

WAITING GAME: The US has so far only offered a ‘best rate tariff,’ which officials assume is about 15 percent, the same as Japan, a person familiar with the matter said Taiwan and the US have completed “technical consultations” regarding tariffs and a finalized rate is expected to be released soon, Executive Yuan spokeswoman Michelle Lee (李慧芝) told a news conference yesterday, as a 90-day pause on US President Donald Trump’s “reciprocal” tariffs is set to expire today. The two countries have reached a “certain degree of consensus” on issues such as tariffs, nontariff trade barriers, trade facilitation, supply chain resilience and economic security, Lee said. They also discussed opportunities for cooperation, investment and procurement, she said. A joint statement is still being negotiated and would be released once the US government has made

‘CRUDE’: The potential countermeasure is in response to South Africa renaming Taiwan’s representative offices and the insistence that it move out of Pretoria Taiwan is considering banning exports of semiconductors to South Africa after the latter unilaterally downgraded and changed the names of Taiwan’s two representative offices, the Ministry of Foreign Affairs (MOFA) said yesterday. On Monday last week, the South African Department of International Relations and Cooperation unilaterally released a statement saying that, as of April 1, the Taipei Liaison Offices in Pretoria and Cape Town had been renamed the “Taipei Commercial Office in Johannesburg” and the “Taipei Commercial Office in Cape Town.” Citing UN General Assembly Resolution 2758, it said that South Africa “recognizes the People’s Republic of China (PRC) as the sole

NEW GEAR: On top of the new Tien Kung IV air defense missiles, the military is expected to place orders for a new combat vehicle next year for delivery in 2028 Mass production of Tien Kung IV (Sky Bow IV) missiles is expected to start next year, with plans to order 122 pods, the Ministry of National Defense’s (MND) latest list of regulated military material showed. The document said that the armed forces would obtain 46 pods of the air defense missiles next year and 76 pods the year after that. The Tien Kung IV is designed to intercept cruise missiles and ballistic missiles to an altitude of 70km, compared with the 60km maximum altitude achieved by the Missile Segment Enhancement variant of PAC-3 systems. A defense source said yesterday that the number of

Taiwanese exports to the US are to be subject to a 20 percent tariff starting on Thursday next week, according to an executive order signed by US President Donald Trump yesterday. The 20 percent levy was the same as the tariffs imposed on Vietnam, Sri Lanka and Bangladesh by Trump. It was higher than the tariffs imposed on Japan, South Korea and the EU (15 percent), as well as those on the Philippines (19 percent). A Taiwan official with knowledge of the matter said it is a "phased" tariff rate, and negotiations would continue. "Once negotiations conclude, Taiwan will obtain a better