Arsonists attacked offices of Greece’s ruling Socialist Party in Athens on Friday as the country suffered a new credit blow ahead of a parliament debate on how to confront its massive debt.

Credit rating agency Standard and Poor’s downgraded two Greek banks and put two others on negative watch. International ratings agencies have delivered a series of heavy blows to Greece’s standing in recent weeks.

Greek Prime Minister George Papandreou has ordered major austerity measures to cut Greece’s 300 billion euro (US$436 billion) debt that has roiled markets and pushed down the euro currency, which Greece shares as a member of the eurozone.

PHOTO: AFP

The attacks on the six Socialist Party offices in Athens came hours after a day of protests by communist-led unions against the austerity measures.

DOWNGRADE

Markets were jolted meanwhile by a new credit downgrade.

Standard and Poor’s cut Eurobank and Alpha Bank to BBB from BBB-plus and placed National Bank of Greece, the country’s biggest private institution, and Bank of Piraeus, its fifth biggest, on negative watch.

S&P downgraded Greek sovereign debt on Wednesday, and Moody’s is expected to issue a judgement by Christmas after warning Greece in October that its grade could be cut.

Papandreou hit out at the power wielded by the agencies and said France and Spain would support him in the matter.

“The Spanish prime minister, for example, says agencies which answer to no one should not be able to make economies rise and fall ... this is not possible in a democratic country with a government elected on a clear program,” ANA quoted Papandreou as saying.

Speaking to reporters in Copenhagen, where he was attending the UN climate change conference, Papandreou said he expected Spanish Prime Minister Jose Luis Rodriguez Zapatero to make the agencies an issue during Spain’s European presidency, which begins next month.

Papandreou also mentioned French President Nicolas Sarkozy.

“He said the agencies which are rating us are the same ones that gave A grades to banks that collapsed the next day,” Papandreou said.

The interest rate which Greece has to pay to attract international savings to finance its overspending, via the bond market, has shot up in recent weeks and is now about twice the rate Germany has to pay.

CREDIBILITY

Greek Finance Minister George Papaconstantinou has just been on a three-day tour of European capitals seeking to salvage Greece’s financial credibility.

He was to lead the Socialist government’s call at a parliament debate yesterday for radical spending cuts to curb the debt and a deficit estimated at 12.7 percent of output.

The government’s targeted cuts already go beyond the planned deficit reduction of 3.6 percent included in next year’s budget.

The finance minister reaffirmed that he wants a bigger cut, saying he was aiming for a “more ambitious reduction” close to 4 percent.

European Central Bank (ECB) Vice President Lucas Papademos meanwhile urged Greek authorities to take “courageous” measures to tackle the swollen fiscal deficit.

Papademos, himself a Greek, said: “These measures would need to be decisive, substantial, and given the magnitude of the problem ... they would have to be courageous.”

Speaking at the ECB’s twice-yearly Financial Stability Review, Papademos further stressed that Britain, Ireland, Spain and the US also had large deficits and that “the issue is really global.”

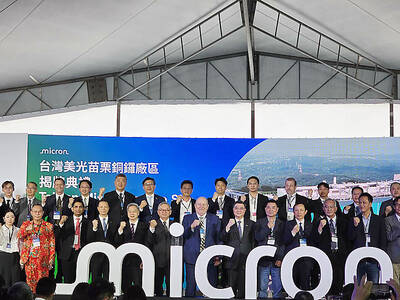

UNPRECEDENTED PACE: Micron Technology has announced plans to expand manufacturing capabilities with the acquisition of a new chip plant in Miaoli Micron Technology Inc unveiled a newly acquired chip plant in Miaoli County yesterday, as the company expands capacity to meet growing demand for advanced DRAM chips, including high-bandwidth memory chips amid the artificial intelligence boom. The plant in Miaoli County’s Tongluo Township (銅鑼), which Micron acquired from Powerchip Semiconductor Manufacturing Corp (力積電) for US$1.8 billion, is expected to make a sizeable capacity contribution to the company from fiscal 2028, the company said in a statement. It would be an extended production site of Micron’s large-scale manufacturing hub in Taichung, the company said. As the global semiconductor industry is racing to reach US$1 trillion

Singapore-based ride-hailing and delivery giant Grab Holdings Ltd has applied for regulatory approval to acquire the Taiwan operations of Germany-based Delivery Hero SE's Foodpanda in a deal valued at about US$600 million. Grab submitted the filing to the Fair Trade Commission on Friday last week, with the transaction subject to regulatory review and approval, the company said in a statement yesterday. Its independent governance structure would help foster a healthy and competitive market in Taiwan if the deal is approved, Grab said. Grab, which is listed on the NASDAQ, said in the filing that US-based Uber Technologies Inc holds about 13 percent of

Taiwan’s food delivery market could undergo a major shift if Singapore-based Grab Holdings Ltd completes its planned acquisition of Delivery Hero SE’s Foodpanda business in Taiwan, industry experts said. Grab on Monday last week announced it would acquire Foodpanda’s Taiwan operations for US$600 million. The deal is expected to be finalized in the second half of this year, with Grab aiming to complete user migration to its platform by the first half of next year. A duopoly between Uber Eats and Foodpanda dominates Taiwan’s delivery market, a structure that has remained intact since the Fair Trade Commission (FTC) blocked Uber Technologies Inc’s

Memory chip stocks extended their losses yesterday after Alphabet Inc’s Google publicized research that could allow more efficient use of the storage needed for artificial intelligence (AI) development. SK Hynix Inc and Samsung Electronics Co, South Korean leaders in the market, fell more than 6 percent and about 5 percent respectively in Seoul. In the US, Micron Technology Inc, Western Digital Corp and Sandisk Corp slid more than 2 percent in pre-market trading, after they all closed lower on Wednesday. Memory companies have been on a tear in recent months as the rapid development of AI infrastructure triggered a spike in chip