Former WorldCom directors have agreed to pay investors US$18 million from their own pocket as part of a settlement of charges against them related to the historic accounting fraud that nearly sank the telephone company, New York Comptroller Alan Hevesi announced Friday.

Ten former WorldCom board members have agreed to pay the money as part of a US$54 million settlement with investors who lost billions as fraud was uncovered, said Hevesi, who as trustee for state employee retirement funds in New York was the lead plaintiff in the case.

The direct payments by the board members -- equaling about one-fifth of each one's personal net worth -- are a highly unusual concession in a securities case.

And yet the deal also marks the third such arrangement in resolving the most egregious corporate scandals of recent years: directors at Enron Corp., Global Crossing Ltd. and now WorldCom have agreed to personally chip in to restore a small fraction of the gigantic losses suffered by investors and employees.

That trend fits in with recent efforts by government regulators and prosecutors to force executives to bear more personal financial responsibility for negligence or wrongdoing.

"This is the best form of deterrence," Bruce Carton, executive director for securities class actions services at Institutional Shareholder Services, a top advisory firm for major investment funds, said Thursday before the deal was announced. "If you can get the individuals who are involved to realize there is a prospect of losing personal wealth if they don't do their jobs, then you will possibly influence behavior."

Typically, all financial penalties relating to a director's alleged negligence or wrongdoing are paid by the company and insurance policies which all corporations take out on behalf of their executives.

The deal, which does not resolve all legal claims in the scandal, comes two weeks before the start of a federal trial against WorldCom chief executive Bernard Ebbers on criminal charges he orchestrated the US$11 billion fraud which pushed the company into bankruptcy in mid-2002. WorldCom emerged from bankruptcy last year and now operates under the name MCI in Ashburn, Virginia.

Legal experts said Thursday the settlement might draw strong objections from several corners. These include the big Wall Street firms still facing WorldCom investor suits, other plaintiffs who haven't resolved their claims against the directors, and the two WorldCom board members who declined to take part in the 10-director deal.

It was not immediately clear how much of the US$18 million each of the 10 directors would pay individually. But since each is to pay a set percentage of his or her personal net worth, the agreement does not assign varying proportions of blame for the scandal, according to a source who spoke on condition of anonymity before Friday's announcement .

The 10 settling former board members are James Allen, Judith Areen, Carl Aycock, Max Bobbitt, Clifford Alexander, Stiles Kellett Jr., Gordon Macklin, John Porter, Lawrence Tucker and the estate of John Sidgmore, who died in 2003, the source said.

Wall Street firms, charged with fraudulent representations when selling WorldCom bonds to investors, may object if they feel the directors are not assigned enough blame in the overall scandal. The greater the percentage of liability attached to the directors, the greater the portion of the overall damages would be considered resolved by their settlement -- and the less the banks might need to pay in a settlement.

Citigroup has already agreed to pay US$2.58 billion to settle its portion of the civil suit. J.P. Morgan Chase & Co., Bank of America Corp. and Deutsche Bank AG remain as defendants.

SETBACK: Apple’s India iPhone push has been disrupted after Foxconn recalled hundreds of Chinese engineers, amid Beijing’s attempts to curb tech transfers Apple Inc assembly partner Hon Hai Precision Industry Co (鴻海精密), also known internationally as Foxconn Technology Group (富士康科技集團), has recalled about 300 Chinese engineers from a factory in India, the latest setback for the iPhone maker’s push to rapidly expand in the country. The extraction of Chinese workers from the factory of Yuzhan Technology (India) Private Ltd, a Hon Hai component unit, in southern Tamil Nadu state, is the second such move in a few months. The company has started flying in Taiwanese engineers to replace staff leaving, people familiar with the matter said, asking not to be named, as the

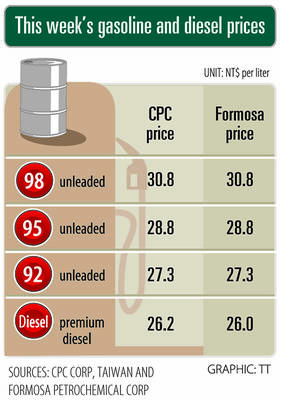

The prices of gasoline and diesel at domestic fuel stations are to rise NT$0.1 and NT$0.4 per liter this week respectively, after international crude oil prices rose last week, CPC Corp, Taiwan (台灣中油) and Formosa Petrochemical Corp (台塑石化) announced yesterday. Effective today, gasoline prices at CPC and Formosa stations are to rise to NT$27.3, NT$28.8 and NT$30.8 per liter for 92, 95 and 98-octane unleaded gasoline respectively, the companies said in separate statements. The price of premium diesel is to rise to NT$26.2 per liter at CPC stations and NT$26 at Formosa pumps, they said. The announcements came after international crude oil prices

STABLE DEMAND: Delta supplies US clients in the aerospace, defense and machinery segments, and expects second-half sales to be similar to the first half Delta Electronics Inc (台達電) expects its US automation business to remain steady in the second half, with no signs of weakening client demand. With demand from US clients remaining solid, its performance in the second half is expected to be similar to that of the first half, Andy Liu (劉佳容), general manager of the company’s industrial automation business group, said on the sidelines of the Taiwan Automation Intelligence and Robot Show in Taipei on Wednesday. The company earlier reported that revenue from its automation business grew 7 percent year-on-year to NT$27.22 billion (US$889.98 million) in the first half, accounting for 11 percent

A German company is putting used electric vehicle batteries to new use by stacking them into fridge-size units that homes and businesses can use to store their excess solar and wind energy. This week, the company Voltfang — which means “catching volts” — opened its first industrial site in Aachen, Germany, near the Belgian and Dutch borders. With about 100 staff, Voltfang says it is the biggest facility of its kind in Europe in the budding sector of refurbishing lithium-ion batteries. Its CEO David Oudsandji hopes it would help Europe’s biggest economy ween itself off fossil fuels and increasingly rely on climate-friendly renewables. While