Earlier this year, word got out about a Visa debit card aimed at people who wanted to borrow money from their 401(k) accounts. With plastic in hand, they could withdraw the funds from an ATM or spend them at any merchant that accepts Visa, just as they could with a regular bank debit card.

The response from normally placid retirement experts was fury so passionate that it actually made you laugh.

"This is an amazingly dumb idea," the president of one 401(k) firm told the Baltimore Sun.

"You can't treat 401[k] participants like adults," a consultant insisted to a trade publication.

"This is close to a predatory lending practice," said a regulator who spoke to Bloomberg News.

Meanwhile, out in Phoenix, Arizona, the family-owned company that manufactures Ping golf clubs takes an entirely different approach to 401(k) fund access. The company's late founder, Karsten Solheim, didn't much care for debt. So the company simply doesn't let its employees borrow against their 401(k)s. Period.

It's tempting to place a halo over the head of Solheim and write the 401(k) debit card off as the spawn of the devil. But these are tricky times. Banks are frantically reducing the credit lines on existing home equity loans. Credit card issuers are deploying similar tactics. That makes 401(k) loans a more attractive option, or sometimes the only remaining one, for people who need money.

Your employer probably doesn't go so far as to ban loans on 401(k) or similar plans altogether, the way Ping's parent company does. It's also unlikely to offer debit card access with its loans anytime soon, because so many people hate the idea.

But examining the rationales for these two extreme approaches is a useful exercise because it helps you figure out whether your own reasons for wanting to borrow hold up. And in the end, your best path may be something between the two extremes: It probably makes sense to have access to your retirement money and dip into it under certain circumstances, though maybe not with a debit card.

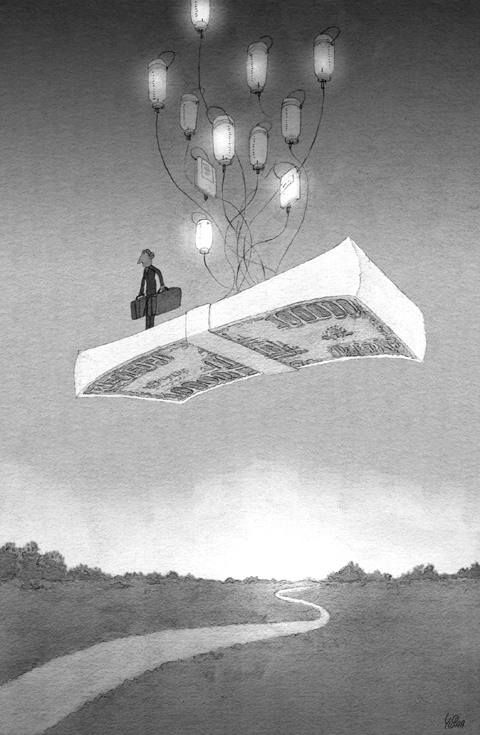

Plenty of people are already borrowing from their 401(k) retirement accounts. The most recent industry surveys show that about 20 percent to 25 percent of eligible employees have outstanding loans.

Never done this yourself? A 401(k) loan lets you borrow from your own retirement account and then pay yourself back, with interest. US federal rules generally allow you to borrow up to 50 percent of your vested 401(k) account balance or US$50,000, whichever is less. Employers can set lower caps if they want.

In most circumstances, you have to repay the loan within five years. Your employer will generally use regular payroll deductions to collect the money and return it to your 401(k). You pay yourself interest, usually the prime rate (currently 5 percent) plus a percentage point or so, depending on your employer.

If you leave the company, it will usually demand full repayment within a month or two. (If you don't comply, you'll generally have to pay income taxes and a penalty on the remaining loan. There are other ways to skip the loan and simply take money out permanently, but I'll save that more radical raid on the retirement kitty for another column.)

Even if you pay a 401(k) loan back in full, it can cost you some serious money in lost investment earnings by the time you retire, based on some calculations that Vanguard performed at my request. For example, a 35-year-old with a US$20,000 balance who takes out two loans during 15 years ends up with about US$38,000 less at age 65 than someone who never borrows, all things being equal.

If you want to test what a loan would cost you, Standard & Poor's has a nice online calculator that runs the numbers for you. It's linked to the version of this column that is posted at nytimes.com/yourmoney.

Given the costs, why are people allowed to borrow against their retirement accounts at all? Over the years, various studies have shown that some people wouldn't save at all or wouldn't save nearly as much if the loans weren't available.

Thus, most big companies allow it, though many small companies don't, in large part because of the administrative hassles of collecting the loan payments. In all, 85 percent of 401(k) participants had access to loans in 2006, the Employee Benefit Research Institute and the Investment Company Institute said.

Though the employees at the Karsten Manufacturing Corp, the makers of Ping products, can't borrow from their 401(k) accounts, it hasn't stopped them from saving money in the first place. The participation rate is a sky-high 92 percent.

There's probably a simple reason for this, though. The company matches each dollar of employee contributions up to the first 5 percent of their salaries, which is generous as employer matches go. That probably helps workers get past any concern about the inability to borrow against their balance.

Stacey Pauwels, a Karsten vice president and granddaughter of the founder, said people often inquire about the ban.

"We're a bit paternalistic as far as the 401(k) loans go," she says. "We don't believe it's in the employees' best interest" to offer them.

The company that issues the 401(k) debit card seems to take the opposite view, that account holders are adults who can be trusted to know when it's appropriate to tap their loan funds.

I say "seems" because I couldn't persuade anyone at the company, Reserve Solutions, a unit of New York City asset manager The Reserve, to comment for this column.

Twelve years ago, when Senator Charles Schumer was a congressman, he heard about a different card-based 401(k) loan product that Bank One was creating. He wrote legislation to stop such use of cards but never pushed the bill through Congress, because Bank One discontinued the program.

When I called the senator's office for comment last week week, a spokesman said that the senator hadn't heard of the Reserve Solutions card until I called. Now, however, the spokesman said, he's planning on bringing back a revised version of his old legislation.

It's too bad that the debit card has gotten so much attention, because there are aspects of Reserve Solutions' system for processing loans that offer some potential improvements on the old-fashioned 401(k) loan repayment system.

For instance, borrowers can take loans in small pieces, which allows them to save on interest. They can pay more than the minimum or standard repayment amount each month. And they don't have to pay all of the loan back immediately upon leaving an employer. It's also a good system for seasonal and other employees who may not have a regular paycheck from which to deduct loan repayments.

I'm with Reserve Solutions on the basic matter of treating people like adults and letting them take loans in the first place. Behaving like an adult, however, means setting some personalized 401(k) loan guidelines and thinking hard about them before borrowing anything.

First, ask yourself how badly you need the money. Putting it toward something that may yield even more money down the road, like a master's degree or a startup for a stay-at-home spouse, is a reasonable bet. A new plasma TV makes less sense.

Then, exhaust all other lower-cost options for borrowing, whether it's a home equity loan or a loan from your family.

If you do turn to your 401(k), don't borrow so much that you can't afford to continue saving money in the plan while you also pay the loan back. Use the calculator I mentioned to see how bad things could get if you borrow a large percentage of your balance, or borrow multiple times, or borrow when you're especially young.

Then, think hard about the tens of thousands of dollars in savings you may not have, as a result of the loan, once you hit retirement age. Are you fine with taking two or three fewer trips once you have more time on your hands? Would you mind not being able to help out as much with a child's student loans or down payment on a home or wedding? What about asking your children for financial help at age 85 because you need special care of some sort?

These are the things you're supposed to be saving for. And borrowing now means you'll have a harder time affording all of them later on.

Could Asia be on the verge of a new wave of nuclear proliferation? A look back at the early history of the North Atlantic Treaty Organization (NATO), which recently celebrated its 75th anniversary, illuminates some reasons for concern in the Indo-Pacific today. US Secretary of Defense Lloyd Austin recently described NATO as “the most powerful and successful alliance in history,” but the organization’s early years were not without challenges. At its inception, the signing of the North Atlantic Treaty marked a sea change in American strategic thinking. The United States had been intent on withdrawing from Europe in the years following

My wife and I spent the week in the interior of Taiwan where Shuyuan spent her childhood. In that town there is a street that functions as an open farmer’s market. Walk along that street, as Shuyuan did yesterday, and it is next to impossible to come home empty-handed. Some mangoes that looked vaguely like others we had seen around here ended up on our table. Shuyuan told how she had bought them from a little old farmer woman from the countryside who said the mangoes were from a very old tree she had on her property. The big surprise

The issue of China’s overcapacity has drawn greater global attention recently, with US Secretary of the Treasury Janet Yellen urging Beijing to address its excess production in key industries during her visit to China last week. Meanwhile in Brussels, European Commission President Ursula von der Leyen last week said that Europe must have a tough talk with China on its perceived overcapacity and unfair trade practices. The remarks by Yellen and Von der Leyen come as China’s economy is undergoing a painful transition. Beijing is trying to steer the world’s second-largest economy out of a COVID-19 slump, the property crisis and

Ursula K. le Guin in The Ones Who Walked Away from Omelas proposed a thought experiment of a utopian city whose existence depended on one child held captive in a dungeon. When taken to extremes, Le Guin suggests, utilitarian logic violates some of our deepest moral intuitions. Even the greatest social goods — peace, harmony and prosperity — are not worth the sacrifice of an innocent person. Former president Chen Shui-bian (陳水扁), since leaving office, has lived an odyssey that has brought him to lows like Le Guin’s dungeon. From late 2008 to 2015 he was imprisoned, much of this