Two years there was a music festival at Knebworth, in central Britain, that was very different. At “Hedgestock” 4,000 hedge fund managers and investors paid US$1,000 a ticket for a weekend of rock’n’roll, champagne, laser clay pigeon shooting and seminars on arcane aspects of how to make even more millions. Some wore beads as part send-up, part veneration of Woodstock, 1960s hippies and “hedgies” bound by the bond of anti-establishment love of liberty, as if the aims of getting stoned and making a fortune gambling in unregulated financial markets were curiously united. The Who played out the event, with proceeds going to the Teenager Cancer Trust.

“Hedgies” were the cool face of capitalism. This year, a rerun of Hedgestock would be pilloried and rightly so. Oil prices are spiraling higher and the plight of stricken banks, property companies and housebuilders is made more acute because of hedge funds’ aggressive speculation. Late last month there were fresh fears that the Western financial order simply could not cope and global stock markets reeled. Hedge funds are emerging as one of the triggers of a first order crisis.

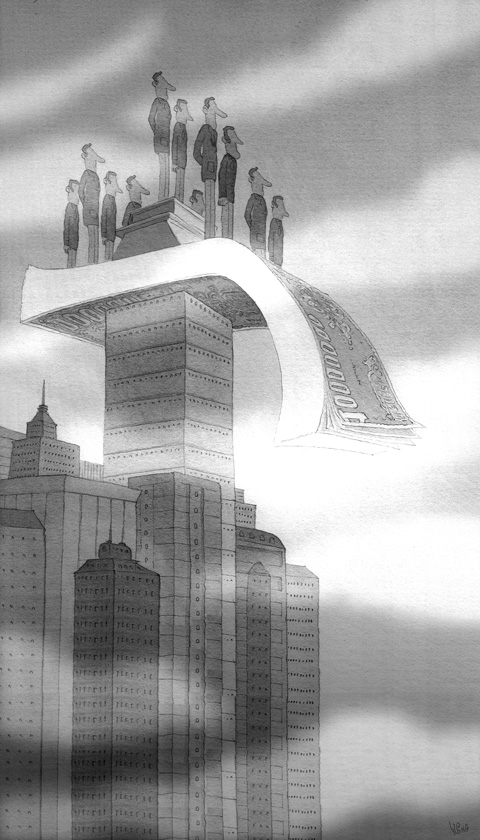

The scale of speculation is eye-poppingly huge. Since Hedgestock, hedge funds have become ever more important. The worldwide industry manages US$2 trillion in assets and a leading hedge fund manager told me they are only a third into their growth cycle — another US$4 trillion is to come. One cynic mocked that the only unifying definition of hedge funds is that they are vehicles to enrich the people risking others’ money; with a 2 percent management fee and a 20 percent share in any investment profits, they certainly do that.

Hedge funds are rich enough to attract any of the great names in investment management and investment banking. New York has more than 120 hedge funds managing more than US$1 billion each, with London running it a close second with more than 80, mainly based in the exclusive areas of Mayfair, Knightsbridge and Belgravia. Some 200 hedge fund partners in London make US$40 million a year, but for the partners who do well, annual earnings can be many times higher. In 2006 Nathaniel Rothschild made US$240 million from his Atticus Capital, while last year George Soros’s Quantum fund returned 32 percent and netted him US$2.9 billion.

Their pitch to investors — from insurance companies to company pension funds, sheiks, Russian oligarchs, the British aristocracy and anybody with sufficient cash — is simple. They set out to make a return of 30 percent a year any way they can in no-holds-barred, hyper-aggressive financial gambling. They take positions in any share, financial instrument or commodity you can name. When they were small you could argue they were a justifiable irritant, challenging and punishing governments and companies alike, who had got themselves into unsustainable financial positions. But now they are becoming the mainstream, degrading the operation of capitalism, turning it into a casino, reducing people’s lives to the chips.

It is fashionable among commentators to regard the UK’s Labour government as the epitome of uselessness, but occasionally there are signs of life. HBOS bank, Britain’s largest mortgage lender, and Bradford & Bingley bank have come under organized attack from hedge funds as they try to raise money from their shareholders. Their shares were being sold to force down the price before being bought back — “short-selling.”

British Chancellor of the Exchequer Alistair Darling and the UK’s Financial Services Authority announced that sellers should disclose their identity. The results are revelatory. The hedge funds were not even buying back the shares, they were “borrowing” them from pension funds to manipulate the market. Ten percent of the shares in Bradford & Bingley were in play, with HBOS only marginally less under siege. Darling flushed the speculative princes of the hedge fund world — Harbinger, Tiger Global Management, GLG — into the open.

A spotlight has been shone on some very murky corners of the financial markets. There practices occur that challenge the very conception of what we consider a company to be, and the accompanying obligations of ownership. A multibillion dollar business has emerged in which shareholders lend their shares to hedge funds to be played with. For a tiny fee, a hedge fund will arrange to borrow shares from a great insurance company or pension fund which it proceeds to sell. Share-loans are believed to exceed a stunning US$15 trillion.

What then happens is the opposite of a bubble, a kind of financial black hole. The hedge funds sell the shares simultaneously and the downward movement becomes self-reinforcing, with companies raising money during a rights issue particularly vulnerable. This is why the government forced disclosure. The hedgies reacted as if they were in Stalin’s Russia; their freedom to kill a company stone dead was being challenged. Let’s not mince words, that is the aim and it gets ugly and personal. A senior UK official told me that in one case some hedge funds had allegedly warned the banks underwriting one rights issue to abandon it or face speculative attack — Mafia practice.

Neither are companies raising money the only target. A visit to the Data Explorers Web site (www.dataexplorers.com) gives you some idea of the extent of the nightmare. For example 10 percent of the shares in UK housebuilder Barratts have been borrowed to be sold. Chief executive Mark Clare said he thought his company was the victim of a sellers’ conspiracy. So it was, and is.

Hedge funds say they are only exposing real frailties and that if the shares are undervalued, long-term investors will buy them. But financial markets do not work like that. They create bubbles and black holes of excess optimism and pessimism, which hedge funds set out to exaggerate. The impact on companies is devastating. British firms no longer have long-term owners who share their long-term mission and purpose. Instead their owners have become their enemies; as Clare says, hardly motivating.

US senators Joseph Lieberman and Susan Collins have been holding hearings to investigate why the oil price is so high. One witness, hedge fund manager Michael Masters, argued that there were two identifiable sources of new demand over the past five years — from China and from speculation — both around the same scale. Without the speculation the oil price would still be below US$100 a barrel.

The senators are proposing that hedge funds, along with other speculators, should be prohibited from oil speculation — and they mention London by name. They said it is hedge funds in London’s unregulated oil futures markets that are making middle America pay twice as much for its gasoline.

That is probably over the top, but there is a truth there. The price of gasoline and the toughness of the credit crunch are being increased by the operation of hedge funds, as is the weakening of your job prospects as companies are forced into ever harsher behavior. It does not have to be like this; the necessary changes in the markets and corporate ownership are fairly easy to make. They would make it harder for some very rich people to get even richer, but in the US and mainland Europe politicians are ready to contemplate that, partly to defend the legitimacy of capitalism itself. Only in Britain is nothing said, a sign, I think, not of our economic maturity, but political emasculation.

Recently, China launched another diplomatic offensive against Taiwan, improperly linking its “one China principle” with UN General Assembly Resolution 2758 to constrain Taiwan’s diplomatic space. After Taiwan’s presidential election on Jan. 13, China persuaded Nauru to sever diplomatic ties with Taiwan. Nauru cited Resolution 2758 in its declaration of the diplomatic break. Subsequently, during the WHO Executive Board meeting that month, Beijing rallied countries including Venezuela, Zimbabwe, Belarus, Egypt, Nicaragua, Sri Lanka, Laos, Russia, Syria and Pakistan to reiterate the “one China principle” in their statements, and assert that “Resolution 2758 has settled the status of Taiwan” to hinder Taiwan’s

The past few months have seen tremendous strides in India’s journey to develop a vibrant semiconductor and electronics ecosystem. The nation’s established prowess in information technology (IT) has earned it much-needed revenue and prestige across the globe. Now, through the convergence of engineering talent, supportive government policies, an expanding market and technologically adaptive entrepreneurship, India is striving to become part of global electronics and semiconductor supply chains. Indian Prime Minister Narendra Modi’s Vision of “Make in India” and “Design in India” has been the guiding force behind the government’s incentive schemes that span skilling, design, fabrication, assembly, testing and packaging, and

Singaporean Prime Minister Lee Hsien Loong’s (李顯龍) decision to step down after 19 years and hand power to his deputy, Lawrence Wong (黃循財), on May 15 was expected — though, perhaps, not so soon. Most political analysts had been eyeing an end-of-year handover, to ensure more time for Wong to study and shadow the role, ahead of general elections that must be called by November next year. Wong — who is currently both deputy prime minister and minister of finance — would need a combination of fresh ideas, wisdom and experience as he writes the nation’s next chapter. The world that

As former president Ma Ying-jeou (馬英九) wrapped up his visit to the People’s Republic of China, he received his share of attention. Certainly, the trip must be seen within the full context of Ma’s life, that is, his eight-year presidency, the Sunflower movement and his failed Economic Cooperation Framework Agreement, as well as his eight years as Taipei mayor with its posturing, accusations of money laundering, and ups and downs. Through all that, basic questions stand out: “What drives Ma? What is his end game?” Having observed and commented on Ma for decades, it is all ironically reminiscent of former US president Harry